Accounting for financial liabilities is not substantially impacted by the adoption of IFRS 9, with one exception

In recent editions of Financial Reporting Insights we have examined the impact that the adoption of IFRS 9 Financial Instruments (“IFRS 9”) will have on accounting for financial assets:- In the mid-June 2018 and late-June 2018 editions we examined the classification and measurement of financial asset

- In the August 2018 edition we examined the impairment of financial assets.

Classification of financial liabilities

Although IFRS 9 will herald major changes in the accounting for financial assets, the accounting for financial liabilities will remain largely consistent with that applied under IAS 39. Under IFRS 9, there will be the same two financial liability classification categories as existed under IAS 39:- Financial liabilities at fair value through profit or loss

- Financial liabilities at amortised cost.

Fair value through profit or loss

A financial liability is classified as a financial liability at fair value through profit or loss if it meets one of the following conditions:- It is held for trading, or

- It is designated by the entity as at fair value through profit or loss (note that such a designation is only permitted if specified conditions are met).

- It is incurred principally for the purpose of repurchasing it in the near term

- On initial recognition it is part of a portfolio of identified financial instruments that are managed together and for which there is evidence of a recent actual pattern of short-term profit-taking, or

- It is a derivative (except for a derivative that is a financial guarantee contract or a designated and effective hedging instrument).

Like IAS 39, IFRS 9 contains a fair value option where entities may designate a financial liability at fair value through profit or loss when doing so results in more relevant information, because either:

- It eliminates, or significantly reduces, a measurement or recognition inconsistency (sometimes referred to as an accounting mismatch) that would otherwise arise from measuring assets or liabilities, or recognising the gains and losses on them, on different bases, or

- A group of financial liabilities, or financial assets and financial liabilities, is managed and its performance is evaluated on a fair value basis, in accordance with a documented risk management or investment strategy, and information about the group is provided internally on that basis to the entity’s key management personnel.

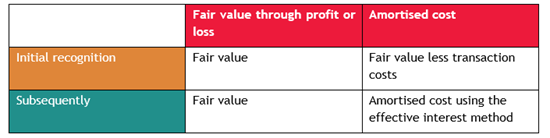

Measurement of financial liabilities

Financial liabilities at fair value through profit or loss are initially recognised at fair value and are thereafter carried at fair value.Financial liabilities at amortised cost are initially recognised at fair value less transaction costs and are thereafter carried at amortised cost using the effective interest method.

Own credit risk

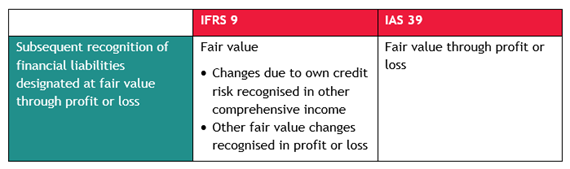

For all financial liabilities at fair value through profit or loss, IFRS 13 Fair Value Measurement requires the measurement of fair value to take into account the effect of the entity’s own credit risk and any other factors that might influence the likelihood that the obligation will or will not be fulfilled.The one major change for financial liabilities designated at fair value through profit or loss relates to the manner in which changes in own credit risk are accounted for.

Under IAS 39, all changes in the fair value of financial liabilities at fair value through profit or loss are recognised in profit or loss. However, under IFRS 9, where a financial liability has been designated at fair value through profit or loss, fair value changes related to changes in the entity’s own credit risk are recognised in other comprehensive income, while all other fair value changes are recognised in profit or loss.

| The requirement to recognise changes in fair value related to the entity’s own credit risk in other comprehensive income does not apply to all financial liabilities measured at fair value through profit or loss, but rather only to financial liabilities designated at fair value through profit or loss. Therefore changes in fair value due to own credit risk for interest rate swaps and other derivatives are recognised in profit or loss. |

The requirement to recognise fair value changes due to an entity’s own credit risk in other comprehensive income is to eliminate the counter-intuitive effect that would otherwise arise (i.e. that the poorer the financial condition of an entity, the higher the discount rate that applies when measuring fair value, resulting in a higher associated gain in profit or loss).

Two-step approach

The requirement to recognise changes in fair value due to an entity’s own credit risk separately in other comprehensive income means that typically a two-step approach is needed:

The difference between the amounts calculated in steps 1 and 2 above will be recognised in profit or loss.

| It should be noted that amounts recognised in other comprehensive income for fair value movements as a result in changes in own credit risk are never recycled to profit or loss when the financial liability is derecognised, but a transfer may be made to another account within equity. |

Example – own credit risk

An entity has a financial liability designated at fair value through profit or loss.The fair value of the liability decreases by $10,000, with $2,000 of that decrease due to a change in the entity’s own credit risk.

Under IAS 39, the journal entry would be:

However, under IFRS 9 the journal entry would be: